Can Bitcoin Solve Our Debt Addiction?

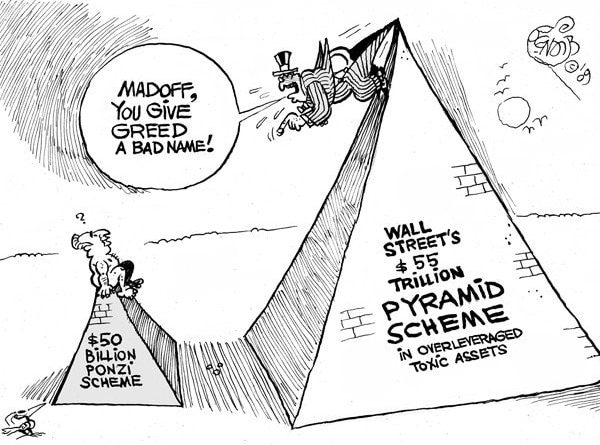

Margarita Groisman graduated from the Georgia Institute of Technology with a degree in industrial engineering and analytics.(Source)Since modern-day commercialisms introduction in the early 19th century, many societies have seen a meteoric rise in wealth and access to cheap products– with the celebration pertaining to an end years later with some sort of major restructuring set off by a major world occasion, such as a pandemic or a war. We see this pattern repeat once again and again: a cycle of debt, high-growth and loaning financial systems; then what we now employ America “a market correction.” These cycles are best described in Ray Dalios “How The Economic Machine Works.” This short article intends to examine whether a new monetary system backed by bitcoin can address our systematic financial obligation concerns constructed into the financial system.There are many examples in history to illustrate the long-term problem with using debt and money printing to fix financial crises. Japans inflation following World War II due to printing money making of financial obligation, the eurozone debt crisis, and what seems to be starting in China, beginning with the Evergrande crisis and property market collapse in rates and unfortunately, many, a lot more cases.Understanding Bankings Reliance On CreditThe basic issue is credit– utilizing money you dont have yet to purchase something you cant manage in cash. We will all likely take on a large amount of financial obligation one day, whether its taking on a home loan to fund a house, handling financial obligation for purchases like automobiles, experiences like college, and so on. Numerous services also utilize big amounts of debt to conduct their everyday business.When a bank offers you a loan for any of these purposes, it deems you as “credit-worthy,” or believes that there is a high opportunity your future revenues and properties combined with your record of payment history will suffice to cover the present expense of your purchase plus interest, so the bank loans you the rest of the money needed to acquire the item with a mutually-agreed upon interest rate and repayment structure.But where did the bank get all that cash for your large purchase or business activities? The bank does not make items or goods and is for that reason creating additional money from these productive activities. Rather, they likewise borrowed this cash (from their lenders who chose to put their cost savings and additional money in the bank). To these lenders, it may feel as if this money is easily offered for them to withdraw anytime. The truth is that the bank lent it out long back, and charged interest fees significantly more than the interest they pay to cash deposits, so they can benefit from the distinction. The bank actually loaned out much more than lenders gave them on the pledge of using their future profits to pay back their loan providers. Upon a savers withdrawal, they just walk around another persons money deposit to ensure you can spend for your purchase immediately. This is undoubtedly an accounting oversimplification, but basically is what happens.Fractional Reserve Banking: The Worlds Biggest Ponzi Scheme?”Madoff and Pyramid Schemes” (Source)Welcome to fractional reserve banking. The truth of the cash multiplier system is that on average, banks loan out 10 times more cash than they really have deposited, and every loan effectively produces cash out of thin air on what is simply a guarantee to pay it back. It is typically forgotten that these personal loans are what really creates brand-new cash. This brand-new money is called “credit” and relies on the assumption that just a very little portion of their depositors will ever withdraw their cash at one time, and the bank will receive all their loans back with interest. If simply more than 10% of the depositors attempt to withdraw their cash simultaneously– for example, something driving customer worry and withdrawal or an economic crisis causing those who have loans not being able to repay them– then the bank stops working or requires to be bailed out.Both of these circumstances have actually occurred numerous times in numerous societies that rely on credit-based systems, though it may be beneficial to take a look at some particular examples and their results.These systems basically have an integrated failure. Eventually, there is an ensured deflationary cycle where the debt must be paid back.Society Pays For The Banks Risky LoansThere is a lot to discuss in terms of how the main bank attempts to stop these deflationary cycles by decreasing the cost for businesses to borrow cash and including newly-printed cash into the system. Basically however, short-term services like this can not work since money can not be printed without losing its worth. When we add new money to the system, the basic result is that we are transferring the wealth of every individual because society to the bleeding bank by reducing the costs power of the entire society. Essentially, that is what occurs throughout inflation: Everyone, consisting of those not initially associated with these credit transactions, gets poorer and has to pay back all the existing credit in the system.The more essential issue is an integrated growth assumption. For this system to work, there should be more students ready to pay for the increasing expenses of college, more individuals aiming to deposit and get loans, more house buyers, more asset development and constant productive enhancement. Development plans like this do not work since ultimately the cash stops coming and individuals do not have power to successfully transfer the costs power of the population to pay these debts like banks do.The system of credit has actually brought numerous societies and individuals into prosperity. However, every society that has actually seen real long-lasting wealth generation has actually seen that it comes through the production of innovative products, technologies, tools and services. This is the only way to produce true long-lasting wealth and bring about development. When we produce products that are brand-new, ingenious and useful that people wish to buy due to the fact that they enhance their lives, we get jointly wealthier as a society. When brand-new companies find ways to make goods we enjoy less expensive, we get jointly wealthier as a society. We get jointly wealthier as a society when companies create incredible experiences and services like making monetary transactions simple and instantaneous. When we try to produce wealth and enormous markets that count on using credit to bank on risky possessions, make market trades and make purchases beyond our current methods, then society stagnates or positions itself on a trajectory towards decline.Would it be possible to approach a system with a more long-lasting concentrated outlook with slower however stable development without the discomfort of severe deflationary cycles? First, extreme and risky credit would need to be eliminated which would imply much slower and less short-term development. Next, our perpetual cash printer would require to end which would lead to extreme discomfort in some areas of the economy.Can Bitcoin Address These Issues?Some say that bitcoin is the option to these problems. If we relocate to a world where bitcoin is not simply a new form of commodity or asset class, however in fact the foundation of a newly-decentralized financial structure, this shift could be a chance to reconstruct our systems to support long-term development and end our addiction to easy credit.Bitcoin is restricted to 21 million coins. No more can ever be developed as soon as we reach the maximum bitcoin in blood circulation. This means that those who own bitcoin might not have their wealth drawn from the easy production of new bitcoin. Looking at the loaning and credit practices of other cryptocurrencies and procedures, they seem to mirror our present systems practices, however with even more risk. In a newly-decentralized financial system, we must make sure we restrict the practice of fractional reserves and highly-leveraged loans and build these brand-new protocols into the exchange procedure itself. Otherwise, there will be no change from the concerns around credit and deflationary cycles as we have now.Cryptocurrency Is Following The Same Path As Traditional BankingIt is just truly great company to loan out money and guarantee returns, and there are numerous companies in the cryptocurrency ecosystem making their own products around extremely dangerous credit. Brendan Greeley writes a persuading argument that loans can not be stopped just by changing to cryptocurrencies in his essay “Bitcoin Can not Replace The Banks:””Creating new credit cash is a good company, which is why, century after century, people have discovered new methods to make loans. The U.S. historian Rebecca Spang points out in her book Stuff and Money in the French Revolution that the monarchy in pre-revolutionary France, to get around usury laws, took lump-sum payments from investors and repaid them in lifetime leas. In 21st-century America, shadow banks pretend they are not banks to prevent regulations. Lending occurs. You cant stop lending. You cant stop it with dispersed computing, or with a stake to the heart. The revenues are simply too excellent.”We saw this happen simply recently with Celsius also, which was a high-yielding loaning product that did essentially what banks do but to a more severe degree by lending out considerably more cryptocurrency than it in fact had with the assumptions that there would not be a large amount of withdrawals simultaneously. When a large amount of withdrawals took place, Celsius needed to halt them because it merely did not have enough for its depositors.So while producing a set restricted supply currency might be an important very first action, it doesnt actually resolve the more essential issues, it simply cuts out the existing anesthetics. The next action towards constructing a system around long-lasting and supported development, presuming future usage of an exchange, is managing the use and standardizing of credit for purchases.Sander van der Hoog offers an extremely helpful breakdown around this in his work “The Limits to Credit Growth: Mitigation Policies And Macroprudential Regulations To Foster Macrofinancial Stability And Sustainable Debt?” In it, he explains the distinction in between two waves of credit: “a main wave of credit to finance developments and a secondary wave of credit to finance overinvestment, speculation and intake.””The reason for this somewhat counter-intuitive outcome is that in the absence of strict liquidity requirements there will be duplicated episodes of credit bubbles. A generic result of our analysis seems to be that a more limiting guideline on the supply of liquidity to companies that are currently highly leveraged is a required requirement for preventing credit bubbles from taking place again and once again.”The clear borders and particular credit guidelines that need to be put in location are beyond the scope of this work, but there must be credit guidelines took into place if there is any hope of sustained growth.While van der Hoogs work is a great location to begin to consider more strict credit guideline, it appears clear that typical credit is a crucial part of development and is most likely to net favorable results if controlled properly; and abnormal credit must be greatly limited with exceptions for limited circumstances in a world run on bitcoin.As we seem to be slowly transitioning into a brand-new currency system, we should make certain that we dont take our old, unhealthy routines and merely convert them into a new format. We need to have integrated stabilizing credit guidelines right into the system, or it will be uncomfortable and too hard to shift out of the dependence on easy money– as it is now. Whether these be constructed into the technology itself or in a layer of policy is yet uncertain and ought to be a topic of significantly more discussion.It seems that we have pertained to just accept that economic downturns and economic crises will simply happen. While we will never have an ideal system, we might undoubtedly be moving toward a more efficient system that promotes long-term maintainable development with the creations of bitcoin as a means of exchange. The suffering triggered to those who can not afford the inflated price of needed products and to those who see their life savings and work disappear throughout crises that are clearly foreseeable and constructed into existing systems do not in fact need to occur if we develop better and more rigorous systems around credit in this brand-new system. We should ensure we do not take our current nasty practices that trigger remarkable pain in the long term and construct them into our future technologies.This is a visitor post by Margarita Groisman. Viewpoints revealed are totally their own and do not always show those of BTC Inc. or Bitcoin Magazine.

Essentially, that is what takes place during inflation: Everyone, consisting of those not initially involved in these credit deals, gets poorer and has to pay back all the existing credit in the system.The more fundamental issue is an integrated growth assumption. Development schemes like this do not work because eventually the cash stops coming and individuals do not have power to efficiently move the spending power of the population to pay these debts like banks do.The system of credit has brought numerous societies and individuals into success. Otherwise, there will be no change from the problems around credit and deflationary cycles as we have now.Cryptocurrency Is Following The Same Path As Traditional BankingIt is simply actually great service to loan out cash and guarantee returns, and there are many business in the cryptocurrency ecosystem making their own products around highly dangerous credit.”The clear borders and specific credit rules that ought to be put in location are outside of the scope of this work, but there should be credit regulations put into location if there is any hope of continual growth.While van der Hoogs work is a great location to begin to think about more stringent credit guideline, it appears clear that normal credit is an important part of growth and is likely to net positive impacts if managed properly; and unusual credit needs to be heavily limited with exceptions for restricted situations in a world run on bitcoin.As we seem to be gradually transitioning into a new currency system, we must make sure that we dont take our old, unhealthy routines and just convert them into a new format. The suffering triggered to those who can not manage the inflated rate of required products and to those who see their life cost savings and work disappear throughout crises that are clearly foreseeable and constructed into existing systems do not actually have to happen if we develop much better and more extensive systems around credit in this brand-new system.