Saylor Junior: A Bitcoin Pleb-Level Speculative Attack

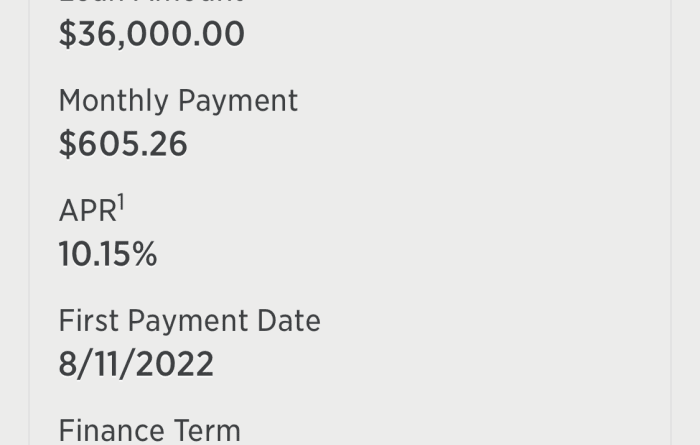

This is a viewpoint editorial by Mickey Koss, a West Point graduate with a degree in economics. He invested four years in the Infantry before transitioning to the Finance Corps.This article is not monetary recommendations– just a financially illiterate psychopath doing some math. As bitcoins price crashes, I discovered myself considering Michael Saylor and his strategic use of debt to outstack basically everyone else worldwide. It got me believing, possibly I could do something similar. A pretty standard dollar-cost averaging (DCA) is an everyday buy to the tune of $20–$25 a day for a pleb on a spending plan. If I were to transform a $20 daily DCA into a financial obligation payment and bring those future sats into the present, the question I had is what it would look like. To compare the 2, I got a quote for an individual loan, getting as close to the $20 a day DCA payment as possible. The real quote is below. The rate at the time of this writing is $22,180. Lets assume a $25,000 bitcoin price, just to add a little conservatism into the calculation. At $25,000, a $36,000 loan will grant you 1.44 bitcoin. If you increase the $605.26 monthly payments by the 84-month loan term, you can see that the loan will cost you $50,841.84. We get a bitcoin price of $35,306.83 for you to break even when compared to the expense of the loan if we divide $50,841.84 by 1.44. If you believe bitcoin will be above $35,000 in seven years, this appears like a pretty excellent deal to me. What about the DCA? A $20 purchase at $25,000 bitcoin is 80,000 sats. If we take the 1.44 BTC above, or 144,000,000 sats, and divide it by the 80,000 sat DCA, you get 1,800. This indicates that at a constant price of $25,000, it would take you 1,800 days to DCA into 1.44 BTC at $20 a day, or 4.9 years. Basically, if bitcoin was to stay at $25,000 or below for the next 5 years, the $20 a day DCA strategy is mathematically much better. However if you think that BTC will normally keep rising over time, it might be useful to transform your DCA into a loan. Even with that 10% rates of interest, bitcoin would just need to exceed $35,000 at the end of the seven-year term for you to come out on top. Truthfully, it appears sort of conservative to me. Michael Saylors strategy is beginning to look quite appealing at these price levels. While I cant, in great conscience, recommend this to anybody, I believed it was an interesting micro example which sheds a little light on where Saylors head might be. Pleased stacking. I constantly love these fire sales. Just to repeat one last time: Definitely do refrain from doing this. This is not financial advice.This is a visitor post by Mickey Koss. Opinions revealed are totally their own and do not always reflect those of BTC Inc. or Bitcoin Magazine.

As bitcoins price crashes, I discovered myself thinking about Michael Saylor and his strategic usage of financial obligation to outstack generally everyone else in the world. Lets presume a $25,000 bitcoin price, simply to add a little conservatism into the calculation. At $25,000, a $36,000 loan will give you 1.44 bitcoin. If we divide $50,841.84 by 1.44, we get a bitcoin price of $35,306.83 for you to break even when compared to the cost of the loan. Basically, if bitcoin was to remain at $25,000 or listed below for the next 5 years, the $20 a day DCA strategy is mathematically much better.