Bitcoin Miners Should Take Solar Energy Plus Storage More Seriously

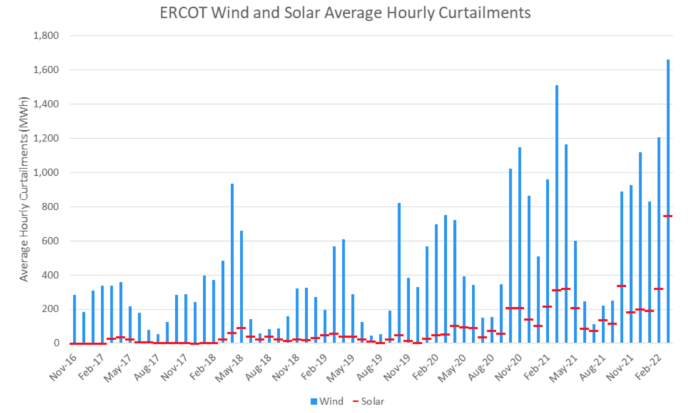

The anti-network result of solar happens in a market when penetration of solar in an area reaches a market-specific tipping point, after which the addition of new solar capability minimizes the benefit (i.e., worth of solar generation) for all solar plants in that market. In its 2021 “Utility Scale Solar” report, LNBL shows this issue in more detail.As solar penetration on a grid increases, the value that solar power can record decreases. The following chart is from a post by Lazard titled “Levelized Cost Of Energy, Levelized Cost Of Storage, And Levelized Cost Of Hydrogen” which shows the fast drop in solar levelized cost of electrical energy: SourceA continued reduction in solar LCOE translates into a downward trajectory of revenues from solar plants. A side note on wind and solar curtailments: Below is a chart from BTU Analytics revealing that wind and solar curtailments are increasing as more intermittent renewables are deployed on the Electric Reliability Council of Texas (ERCOT) grid. The brand-new incentive plus the financial investment in U.S.-based production of solar and batteries is poised to make the U.S. the leading country in solar and storage power plants.

This is an opinion editorial by Ali Chehrehsaz, a mechanical engineer with 16 years of experience in the energy industry.This post will describe how gathering solar power and keeping it can provide a powerful dynamic for bitcoin mining operations by outlining that: Hybrid power plants that match electrical generation, particularly solar, with batteries are growing rapidlyBitcoin mining will be incorporated in these plants together with batteries, for the very same reasonsIncorporating bitcoin mining in addition to batteries requires correct sizing of released properties, and also splitting energy between batteries, mining and the grid in a method that enhances revenueThe course forward will not be technically or commercially basic, but the opportunity is enormous Hybrid Power PlantsThere is a new type of power plant rising: batteries are being co-located with wind, solar photovoltaic (“PV”), nonrenewable fuel sources, etc to develop what are referred to as “hybrid power plants.” Amongst these hybrid power plants, solar-plus-battery plants are the fastest-growing section. Lawrence Berkeley National Labs (LBNL) recently published findings in a briefing titled “2021 Was A Big Year For Hybrid Power Plants– Especially PV+S torage.” In the article, it pointed out: “Among the functional generator+storage hybrids, PV+storage dominates in terms of plant number (140 ), storage capacity (2.2 GW [gigawatts]/ 7.0 GWh [gigawatt hours], storage: generator capacity ratio (53%), and storage duration (3.2 hours). “SourceThe briefing goes on to state that: “Last year was a breakout year for PV+storage hybrids in particular: 67 of the 74 hybrids included in 2021 were PV+storage. By the end of 2021, there was more GW of battery capacity operating in PV+storage hybrids (2.2 GW) than as standalone storage plants (1.8 GW). Much of the battery capability included hybrid kind in 2021 was a battery retrofit to a pre-existing PV plant.” This last point is noteworthy, and we will return to discuss it later on. SourceThis pattern is continuing and, as the article explains, there were more than 670 GW of solar plants in the interconnection lines in the U.S. since the end of 2021. SourcePrisoners Of Time And GeographyWhy are batteries being contributed to solar plants at such a quick rate? There are two factors at play: deflation in the value available for solar energy and the ever-increasing competitiveness within the solar market. Problem One: Solar Value Deflation What is solar value deflation? The LBNL instruction supplies a hint: “… [PV+storage] can be discovered throughout much of the nation … though the biggest such plants are in California and the West …” In a word: location. Solar power in areas like California, Nevada and Arizona is suffering from an anti-network effect. The anti-network result of solar occurs in a market when penetration of solar in a place reaches a market-specific tipping point, after which the addition of new solar capacity minimizes the advantage (i.e., worth of solar generation) for all solar plants because market. In its 2021 “Utility Scale Solar” report, LNBL demonstrates this issue in more detail.As solar penetration on a grid increases, the worth that solar energy can record declines. This leads us to another hint: time. The hours throughout which any provided solar generator can produce electrical power are, by definition, the exact same hours that every other nearby solar generator can produce electricity, which end up ending up being the hours for which the market is oversupplied and costs are lower. This is why renewables are, in a way, detainees of time and geography. See the example of California laid out by LNBL: At 22% penetration, solar energy can just catch 75% of the worth of generation with a baseload 24/7 power profile. The issue is already noticeable in other markets at penetrations as low as 5%. All markets are heading in this instructions. Owners of existing or planned solar projects require to discover ways to hedge this danger and diversify their revenue streams. Issue Two: Extreme Competition The other aspect is the success of solar, creating an exceptionally competitive industry that is now challenging additional development. The solar market began much behind other power generation markets and has needed to reach earn its share of the power generation mix. The industry has been utilizing the levelized expense of energy (LCOE) metric to compare its costs to coal, gas and other generation sources. Solar ended up being the lowest LCOE kind of generation in the last decade and this has actually been driving the incredible growth of solar capability. But the competitors with other generation sources continues within the industry itself, producing a race to the bottom which is deteriorating the returns for financiers in solar. The following chart is from an article by Lazard entitled “Levelized Cost Of Energy, Levelized Cost Of Storage, And Levelized Cost Of Hydrogen” which shows the fast drop in solar levelized expense of electrical power: SourceA continued reduction in solar LCOE equates into a downward trajectory of revenues from solar plants. Investors in solar are looking for ways to increase profits within the confines of the power market. Batteries are one such technology that offers a path to higher incomes through arbitrage, demand action and supplementary services. The Roadmap For Bitcoin MinersWhat is the opportunity for bitcoin miners? The manner in which storage has actually dovetailed neatly into the solar worth stack supplies a beneficial roadmap for bitcoin miners to follow. Bitcoin mining can likewise offer similar chances for solar plants to gain access to greater revenues by running as a flexible resource for the grid. Since batteries have actually a fixed storage capacity and provide a short-term energy arbitrage opportunity against the regional power grid, ultimately, even a battery must take the local grid market costs. Bitcoin mining has no storage limit (allowing long-lasting arbitrage) and can supply arbitrage anywhere on the world (more on that subject: “Bitcoin Is The First Global Market For Electricity”). The pairing of bitcoin mining and solar is easy in concept but making the physics and financing work in practice is challenging. To create accretive returns, Bitcoin miners need to precisely size their releases when co-locating with solar and battery hybrid plants. The co-location strategy requires an understanding and forecast of the volume of electrical energy production from the solar plant and the associated worth of each unit of energy produced by the plant. This need to be done on both a long-term and a short-term (near real-time) basis, to support design/investment and operations. In addition to the probabilistic production volume of solar, knowing the value of energy at each period should be comprehended (e.g., five-minute duration); e.g., worth can differ widely and sometimes can reach $0 per kilowatt hour (kWh) due to curtailments. A side note on wind and solar curtailments: Below is a chart from BTU Analytics revealing that wind and solar curtailments are increasing as more intermittent renewables are released on the Electric Reliability Council of Texas (ERCOT) grid. The most impacted wind and solar plants saw 29% and 21% (respectively) of their total yearly generation reduced in 2021 to 2022! Source Co-optimization for integrating bitcoin mining is an obstacle worth solving for miners provided the increase of solar and battery hybrid plants in the mix of new generation sources. This pattern is likely to grow at a rapid rate.In summary, increasing deflation in worth and increase in competitors of solar have incentivized the pairing of batteries with existing solar plants. Now there is a new reward that will accelerate the development of battery paired hybrid plants. What we have actually seen to date has actually occurred within the pre– Inflation Reduction Act (IRA) age. The IRA freshly permits a 30% investment tax credit (ITC) incentive for standalone batteries over the next 10 years which will improve the redevelopment of existing solar plants to become hybrid plants. As mentioned earlier, battery retrofit to existing solar plants is an emerging sector. This section will grow even much faster over the next years with the new ITC reward. The new incentive plus the financial investment in U.S.-based production of solar and batteries is poised to make the U.S. the leading nation in solar and storage power plants. Bitcoin miners have a huge opportunity to use one of the most quickly growing types of energy generation by figuring out the physics and finance of co-locating with solar and storage power plants. This is a visitor post by Ali Chehrehsaz. Viewpoints revealed are completely their own and do not necessarily show those of BTC Inc or Bitcoin Magazine.