Understanding Our Current Monetary System And Bitcoin’s Value Proposition

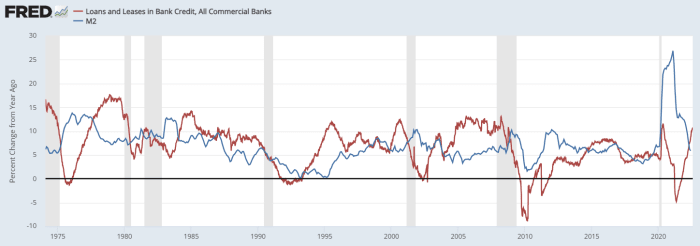

This is a viewpoint editorial by Taimur Ahmad, a graduate student at Stanford University, concentrating on energy, environmental policy and global politics.Authors note: This is the first part of a three-part publication. Part 1 presents the Bitcoin standard and assesses Bitcoin as an inflation hedge, going deeper into the principle of inflation. Part 2 focuses on the existing fiat system, how cash is created, what the cash supply starts and is to discuss bitcoin as cash. Part 3 looks into the history of cash, its relationship to state and society, inflation in the Global South, the progressive case for/against Bitcoin as money and alternative use-cases. Bitcoin As Money: Progressivism, Neoclassical Economics, And Alternatives Part II “Everyone can develop cash; the problem is to get it accepted”– Hyman Minsky * The following is a direct extension of a list from the previous piece in this series. 3. Money, Money Supply And Banking Now onto the 3rd point that gets everyone riled up on Twitter: What is cash, what is cash printing and what is the cash supply? Let me start by saying that the first argument that made me crucial of the political economy of Bitcoin-as-money was the infamous, sacrilegious chart that reveals that the U.S. dollar has lost 99% of its worth gradually. The majority of Bitcoiners, including Michael Saylor and co., love to share this as the bedrock of the argument for bitcoin as money. Cash supply goes up, worth of the dollar boils down– currency debasement at the hands of the federal government, as the story goes. Source: Visual CapitalistI have currently described in Part 1 what I consider the relationship in between cash supply and costs, however here I d like to go one level deeper.Lets start with what cash is. It is a claim on genuine resources. In spite of the extreme, objected to debates across historians, anthropologists, economists, ecologists, philosophers, and so on, about what counts as cash or its dynamics, I believe it is affordable to assume that the underlying claim throughout the board is that it is a thing that permits the holder to procure services and products. With this background then, it does not make good sense to take a look at an isolated worth of money. Actually though, how can somebody show the value of cash in and of itself (e.g., the worth of the dollar is down 99%)? Its worth is only relative to something, either other currencies or the quantity of products and services that can be obtained. The fatalistic chart showing the debasement of fiat does not say anything. What matters is the buying power of customers utilizing that fiat currency, as earnings and other social relations denominated in fiat currency also move synchronously. Are U.S. customers able to acquire 99% less with their salaries? Obviously not.The counterarguments to this usually are that wages do not stay up to date with inflation and that over the short-medium term, money cost savings decline which hurts the working class as it doesnt have access to high yielding financial investments. Real salaries in the U.S. have actually been continuous considering that the early 1970s, which in and of itself is a major socioeconomic issue. There is no direct causal link in between the expansionary nature of fiat and this wage pattern. The 1970s were the start of the neoliberal regime under which labor power was crushed, economies were deregulated in favor of capital and industrial jobs were contracted out to underpaid and exploited employees in the Global South. I digress. Lets return to the what is money question. Apart from a claim over resources, is money likewise a shop of value over the medium term? Once again, I desire to be clear that I am talking only about industrialized nations so far, where devaluation isnt a genuine thing so buying power doesnt erode over night. I d argue that it is not the role of money– money and its equivalents like bank deposits– to function as a store of value over the medium-long term. It is expected to act as a cash which needs rate stability just in the short run, combined with anticipated and progressive devaluation in time. Combining both functions– a highly liquid, exchangeable property and a long-lasting cost savings system– into something generates income a complex, and possibly even inconsistent, idea. To safeguard acquiring power, access to monetary services requires to be expanded so that people have access to reasonably safe properties that keep up with inflation. Concentration of the financial sector into a handful of large players driven by profit intention alone is a significant impediment to this. There is no fundamental factor that an inflationary fiat currency needs to cause a loss of buying power time, particularly when, as argued in Part 1, price changes can take place since of multiple non-monetary reasons. Our socioeconomic setup, by which I mean the power of labor to work out salaries, what occurs to profit, etc, needs to enable purchasing power to increase. Lets not forget that in the post-WWII era this was being accomplished although money supply was not growing (formally the U.S. was under the gold requirement however we know it was not being imposed, which resulted in Nixon moving away from the system in 1971). Okay so where does cash come from and were 40% of dollars printed throughout the 2020 federal government stimulus, as is commonly declared? Neoclassical economics, which the Bitcoin basic story utilizes at numerous levels, argues that the government either borrows money by offering debt, or that it prints cash. Banks lend money based upon deposits by their customers (savers), with fractional reserve banking allowing banks to lend multiples higher than what is transferred. It comes as no surprise to anyone who is still reading that I d argue both these concepts are incorrect. Heres the appropriate story which (trigger caution once again) is MMT based– credit where its due– but concurred to by bond investors and monetary market specialists, even if they disagree on the ramifications. The federal government has a monopoly on money development through its position as the sovereign. It develops the national currency, enforces taxes and fines in it and uses its political authority to secure versus fake. There are 2 distinct ways in which The State connects with the financial system: one, through the reserve bank, it provides liquidity to the banking system. The central bank does not “print cash” as we colloquially understand it, rather it creates bank reserves, a special type of money that isnt truly cash that is used to purchase items and services in the real economy. These are assets for commercial banks that are used for inter-bank operations. Quantitative easing (those scary big numbers that the reserve bank announces it is injecting by buying bonds) is unconditionally not money printing, however merely reserve banks swapping interest bearing bonds with bank reserves, a net neutral transaction as far as the money supply is worried although the reserve bank balance sheet broadens. It does have an influence on asset costs through numerous indirect mechanisms, however I will not go into the information here and will let this terrific thread by Alfonso Peccatiello (@MacroAlf on Twitter) describe. So the next time you become aware of the Fed “printing trillions” or expanding its balance sheet by X trillion, just think of whether you are really discussing reserves, which once again do not enter the real economy so do not contribute to “more cash going after the same amount of items” story, or real cash in blood circulation. Two, the federal government can likewise, through the Treasury, or its comparable, produce money (typical people money) that is distributed through the governments bank– the central bank. The modus operandi for this operation is usually as follows: Say the federal government decides to send out a one-time money transfer to all residents. The Treasury authorizes that payment and jobs the main bank to perform it.The reserve bank marks up the account that each business bank has at the reserve bank (all digital, simply numbers on a screen– these are reserves being developed). the commercial banks correspondingly increase the accounts of their customers (this is money being produced). customers/citizens get more cash to spend/save. This type of government costs (financial policy) straight injects money into the economy and is thus unique from financial policy. Direct cash transfers, welfare, payments to vendors, and so on, are examples of financial spending. Many of what we call money, however, is developed by industrial banks straight. Banks are certified representatives of The State, to which The State has extended its powers of money creation, and they produce cash out of thin air, unconstrained by reserves, every time a loan is made. Such is the magic of double-entry accounting, a practice that has actually been in usage for centuries, where cash enters being as a liability for the issuer and a property for the receiver, netting out to no. And to reiterate, banks do not need a specific amount of deposits to make these loans. Loans are made based on whether the bank thinks it makes economic sense to do so– if it requires reserves to fulfill guidelines, it simply borrows them from the central bank. There are capital, not reserve, restraints on loaning however those are beyond the scope of this piece. The main factor to consider for banks in making loans/creating money is earnings maximization, not whether it has enough deposits in its vault. Banks are producing deposits by making loans.This is an essential shift in the story. My analogy for this is parents (neoclassical economists) telling kids a phony birds and bees story in action to the concern of where infants come from. Rather, they never correct it causing an adult citizenry running around without learning about recreation. This is why the majority of people still speak about fractional reserve banking or there being some naturally repaired supply of cash that the personal and public sectors compete over, because thats what econ 101 teaches us.Lets review the idea of cash supply now. Provided that many of the cash in flow comes from the banking sector, and that this cash creation is not constrained by deposits, it is sensible to claim that the stock of money in the economy is not simply driven by supply, but by need. If people and services are not demanding new loans, banks are not able to produce brand-new money. This has a cooperative relationship with the service cycle, as cash production is driven by expectations and market outlook however likewise drives financial investment and growth of output. The chart below shows a procedure of bank financing compared to M2. While the two have a positive connection, it does not always hold, as is glaringly apparent in 2020. Even though M2 was rising greater post-pandemic, banks were not providing due to unsure economic conditions. As far as inflation is worried, there is the included complexity of what banks are providing for, i.e., whether those loans are being utilized for efficient ends, which would increase financial output or ineffective ends, which would end up resulting in (asset) inflation. This decision is not driven by the government, however by the private sector.The last issue to add here is that while the above metrics serve as helpful steps for what takes place within the United States economy, they do not catch the cash production that takes place in the eurodollar market (eurodollars have absolutely nothing to do with the euro, they just refer to the existence of USD outside the U.S. economy). Jeff Snider provided an outstanding run through of this during his appearance on the What Bitcoin Did podcast for anyone who wants a deep-dive, but essentially this is a network of banks that operate outside the U.S., are not under the formal jurisdiction of any regulatory authority and have the license to produce U.S. dollars in foreign markets. This is since the USD is the reserve currency and needed for worldwide trade between two parties that might not have anything to do with the U.S. even. For example, a French bank might release a loan denominated in U.S. dollars to a Korean company wanting to purchase copper from a Chilean miner. The quantity of money developed in this market is anybodys guess and hence, a true step of the cash supply is not even practical. This is what Alan Greenspan had to state in a 2000 FOMC conference: “The problem is that we can not extract from our analytical database what is true cash conceptually, either in the transactions mode or the store-of-value mode.” Here he refers not just to the Eurodollar system but also the proliferation of complicated monetary items that occupy the shadow banking system. Its hard to speak about cash supply when its hard to even specify money, provided the prevalence of money-like alternatives. For that reason, the argument that government intervention through monetary and fiscal expansion drives inflation is just not true as most of the cash in flow is outside the direct control of the federal government. Could the government get too hot the economy through overspending? Sure. That is not some predefined relationship and is subject to the state of the economy, expectations, etc.The concept that the federal government is printing trillions of dollars and debasing its currency is, to no ones surprise at this point, simply not true. Only taking a look at financial intervention by the federal government presents an incomplete image as that injection of liquidity could be, and in a lot of cases is, offseting the loss of liquidity in the shadow banking sector. Inflation is a complex subject, driven by customer expectations, business pricing power, cash in circulation, supply chain interruptions, energy costs, etc. It can not and ought to not be just lowered to a financial phenomenon, specifically not by looking at something as one-dimensional as the M2 chart. The economy should be seen, as the post-Keynesians revealed, as interlocking balance sheets. This holds true merely through accounting identity– somebodys property needs to be somebody elses liability. When we talk about paying back the financial obligation or lowering government spending, the concern needs to be what other balance sheets get affected and how. Let me give a streamlined example: in the 1990s throughout the Clinton era, the U.S. government commemorated budget surpluses and paying back its national financial obligation. Because by meaning somebody else had to be getting more indebted, the U.S. family sector racked up more debt. And since households could not develop cash while the federal government could, that increased the overall risk in the monetary sector.Bitcoin As MoneyI can think of the individuals reading till now (if you made it this far) saying “Bitcoin fixes this!” because its transparent, has a set issuance rate and a supply cap of 21 million. Here I have both philosophic and financial arguments when it comes to why these features, regardless of the existing state of fiat currency, are not the exceptional solution that they are explained to be. The very first thing to note here is that, as this piece has actually ideally shown so far, that since the rate of change of cash supply is not equivalent to inflation, inflation under BTC is programmatic or not transparent and will still undergo the forces of demand and supply, power of the rate setters, exogenous shocks, etc. Cash is the grease that permits the cogs of the economy to churn without excessive friction. It streams to sectors of the economy that require more of it, enables new avenues to establish and acts as a system that, ideally, straighten out wrinkles. The Bitcoin basic argument rests on the neoclassical assumption that the government controls (or controls, as Bitcoiners call it) the cash supply which battling away this power would lead to some real kind of a financial system. Our present monetary system is mostly run by a network of private stars that The State has bit, arguably too little, control over, despite these stars benefitting from The State acting and guaranteeing deposits as the lending institution of last resort. And yes, of course elite capture of The State makes the nexus in between monetary institutions and the government culpable for this mess.But even if we take the Hayekian approach, which concentrates on decentralizing control totally and utilizing the collective intelligence of society, countering the current system with these features of Bitcoin falls under the technocratic end of the spectrum since they are prescriptive and create rigidity. Should there be a cap on money supply? What is the proper issuance of brand-new cash? Should this hold in all circumstances agnostic of other socioeconomic conditions? Pretending that Satoshi in some way was able to address all these questions across time and area, to the degree that no one should make any changes, seems remarkably technocratic for a community that is discussing the “peoples cash” and freedom from the tyranny of experts.Bitcoin is not democratic and not managed by the people, despite it using a low barrier to enter the financial system. Simply because it is not centrally governed and the guidelines cant be altered by a small minority does not, by meaning, imply Bitcoin is some bottom-up form of cash. It is not neutral money either due to the fact that the option to develop a system that has a fixed supply is a political and subjective choice of what money need to be, instead of some a priori exceptional quality. Some advocates may state that, if need be, Bitcoin can be altered through the action of the bulk, however as soon as this door is opened, concerns of politics, equality and justice flood back in, taking this discussion back to the start of history. This is not to state that these features are not important– certainly they are, as I argue later on, however for other use-cases. For that reason, my contentions thus far have actually been that: Understanding the money supply is made complex since of the monetary intricacy at play.The cash supply does not always cause inflation.Governments do not manage the cash supply and that reserve bank cash (reserves) are not the exact same thing as money.Inflationary currencies do not always lead to a loss of buying power, which that depends more on the socioeconomic setup.An endogenous, elastic money supply is essential to get used to financial changes.Bitcoin is not democratic cash just although its governance is decentralized. In Part 3, I discuss the history of money and its relationship with the state, examine other conceptual arguments that underpin the Bitcoin Standard, supply a perspective on the Global South, and present alternative use-cases. This is a guest post by Taimur Ahmad. Viewpoints revealed are entirely their own and do not always show those of BTC, Inc. or Bitcoin Magazine.

Part 2 focuses on the present fiat system, how cash is developed, what the cash supply starts and is to comment on bitcoin as cash. Cash, Money Supply And Banking Now onto the third point that gets everyone riled up on Twitter: What is cash, what is cash printing and what is the money supply? The main bank does not “print cash” as we informally understand it, rather it produces bank reserves, a special kind of money that isnt actually cash that is utilized to buy items and services in the genuine economy. Provided that many of the cash in circulation comes from the banking sector, and that this money production is not constrained by deposits, it is reasonable to declare that the stock of money in the economy is not just driven by supply, however by demand. My contentions hence far have actually been that: Understanding the money supply is complicated due to the fact that of the monetary complexity at play.The cash supply does not always lead to inflation.Governments do not manage the money supply and that central bank money (reserves) are not the exact same thing as money.Inflationary currencies do not necessarily lead to a loss of acquiring power, and that depends more on the socioeconomic setup.An endogenous, flexible money supply is required to change to economic changes.Bitcoin is not democratic cash simply even though its governance is decentralized.