Jerome Powell Contradicts Fed’s Own Statement, Chaos Ensues

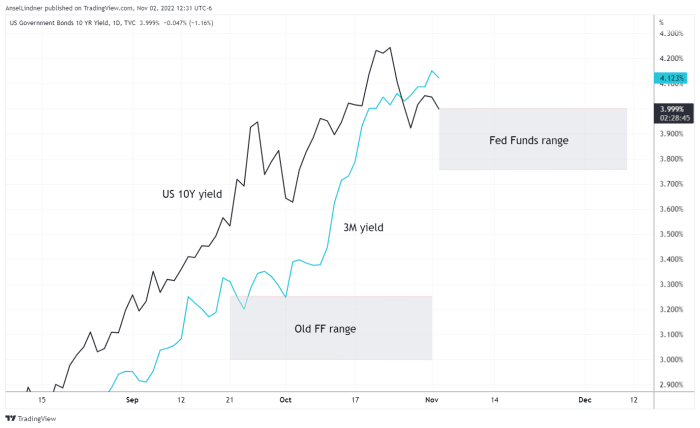

We discuss the diesel scarcity brewing on the east coast of the U.S.Federal Reserve FOMC Raises Rates AgainCK and I agree that the level of significance of the Federal Reserve and the FOMC policy decision to the market is an indication of an extremely unhealthy economy, where main bank decisions are the only video game in town.The Fed raised interest rates by 75 basis points (bps) to a brand-new Fed Funds target range of 3.75% to 4%. The market had actually been forecasting the Fed to not pivot away from their course in this meeting, despite the global liquidity concerns appearing in the financial system.The central bank maintained their policy trajectory, but the statement did include some softening of their hawkish tone. If the Fed can send out combined messages and keep the market unsure, the effects of their last couple of walkings can be more significant.ChartsThe charts on Fed Day were moving quickly. Bitcoin and stocks headed down, the dollar up.The one chart I will consist of on this companion post to the podcast is that of the 3-month and 10-year Treasury rates revealing the most crucial inversion in the curve.3-month and 10-year Treasury securities, in relation to the Fed Funds target rangeWhat you can discover on this chart is the 3-month yield going higher than the 10-year yield. The 10-year yield is terribly close to being inside the Fed Funds target range.What Ive been stating for months is that the Fed will continue to raise rates until the market forces them to stop.

“Fed Watch” is a macro podcast, real to bitcoins rebel nature. In each episode, we question mainstream and Bitcoin narratives by examining existing events in macro from across the globe, with an emphasis on reserve banks and currencies.Watch This Episode On YouTube Or RumbleListen To The Episode Here: In this episode, CK and I cover Jerome Powell and the FOMC policy choice in depth, evaluating declarations from the Federal Reserve, Powell and other economists. Then we move onto charts, starting with bitcoin and the dollar, then proceeding to Treasury rates. Last but not least, we go over the diesel shortage brewing on the east coast of the U.S.Federal Reserve FOMC Raises Rates AgainCK and I concur that the level of significance of the Federal Reserve and the FOMC policy decision to the market signifies a very unhealthy economy, where reserve bank choices are the only video game in town.The Fed raised interest rates by 75 basis points (bps) to a new Fed Funds target series of 3.75% to 4%. This was not a surprise. The marketplace had actually been anticipating the Fed to not pivot far from their course in this conference, in spite of the worldwide liquidity concerns appearing in the monetary system.The reserve bank kept their policy trajectory, but the declaration did include some softening of their hawkish tone. The sentence that leaps out is the following:”In identifying the pace of future boosts in the target variety, the Committee will take into consideration the cumulative tightening of monetary policy, the lags with which financial policy impacts economic activity and inflation, and monetary and economic advancements.””Cumulative” is the word individuals are concentrating on. What does “cumulative” mean in this context? The Fed is putting their meeting-to-meeting decisions within a wider scope of their tightening up program as a whole given that March 2022, in addition to considering their internationally crucial role. The thinking Powell depicts in the press conference that followed is blended. They desire to put their decisions within an entire program, however also want to be information based on a meeting-to-meeting basis.Overall, I believe that their intention is to cause unpredictability. Unpredictability is essential at the end of a hiking cycle. The Federal Reserves objective is to cause a financial slowdown to bring need down to remain in line with supply, but they cant do that if the marketplace is frontrunning completion of the hiking cycle. Thats precisely what weve seen over the last several months. Im sure Powell has actually mixed sensations about the stock exchange staying resistant to their hiking, with the S&P 500 above where it was at the time of the June conferences hike. That was 3 conferences with 75 bps walkings, the other day made it 4, and yet the stock market was higher. He wants a “soft landing”– to achieve their policy objectives without significant damage to the economy– however at the very same time their objective is to damage the economy. Its a contradictory tightrope they are trying to walk.The intentions of the last couple of walkings in the tightening program can not be achieved if the market is frontrunning their downturn, the pause, and after that the eventual turnaround. This is where the purposeful unpredictability is available in. The effects of their last couple of hikes can be more significant.ChartsThe charts on Fed Day were moving rapidly if the Fed can send out mixed messages and keep the market uncertain. I postponed taking snapshots until 30 minutes after the Feds statement, however the blended messaging from Powell triggered them to swing wildly. I will not publish them here since they are already out of date, but you can look at them on the slide deck for this episode.The initial reaction was constant across the board. Markets took the written declaration, including the brand-new language about cumulative effects, as a dovish pivot. Bitcoin spiked together with stocks and the dollar moved down.However, as quickly as Powell began to take concerns at journalism conference, and with his mixed messaging detailed above, markets reversed. Bitcoin and stocks headed down, the dollar up.The one chart I will include on this companion post to the podcast is that of the 3-month and 10-year Treasury rates revealing the most important inversion in the curve.3-month and 10-year Treasury securities, in relation to the Fed Funds target rangeWhat you can discover on this chart is the 3-month yield going greater than the 10-year yield. Likewise, the 10-year yield is extremely close to being inside the Fed Funds target range.What Ive been stating for months is that the Fed will continue to raise rates up until the marketplace forces them to stop. That force applied by the market will show up as longer term rates just not complying with the Fed anymore and going lower, like we can see with the 10-year yield here.The Fed is admittedly “information reliant.” They tell us they are followers, but if you wish to know where the Fed is going, all you have to do is look at the yields. If government security yields begin heading down into the Fed Funds target variety, by the next meeting their options will be: raise rates once again and lose confidence that they are in control of anything, or pause, or even do a “mid-cycle adjustment” and decrease them. Powell has done what he calls a mid-cycle change before. Back in 2019, the first rate cut in July was downplayed as simply such a relocation. Naturally, it was then followed by enormous cuts in the following months.Diesel ShortageThere are other things occurring in the economy than the Federal Reserve. There is concern about diesel scarcities in the U.S. Reports are flying about there being only a couple weeks of diesel left in storage, and with the winter season beginning, diesel and heating oil need is set to increase.To cover this story, I read from a terrific article by Tsvetana Paraskova. She covers the shortage and factors behind it in terrific detail.In brief, U.S. refinery capacity is down due to some plants being switched to making biofuel and our imports from Russia are non-existent due to crazy sanctions.On the program, we get sidetracked since I am not personally that anxious about the diesel lack. It will trigger some pain, but the solution is through that discomfort. Greater rates will trigger one of 2 things to occur– or both: greater rates will stimulate more production or higher costs will trigger political changes to enable greater production.There is a nearly universal fear of greater costs and they are demonized as “inflation” at every turn. Obviously, high costs arent bad if you are a producer. They arent bad in general, either. Costs are supposed to be neutral and give you information about the economy. The only price modifications that are a net negative are those due to changes in the cash supply. Since our present financial condition is not due to money printing but instead supply crises and bad government policies, the cost increases are required to fix the issues today.This is a visitor post by Ansel Lindner. Viewpoints revealed are totally their own and do not always show those of BTC Inc. or Bitcoin Magazine.