Central banks will face unfamiliar challenges to achieve CBDC inclusivity, study says

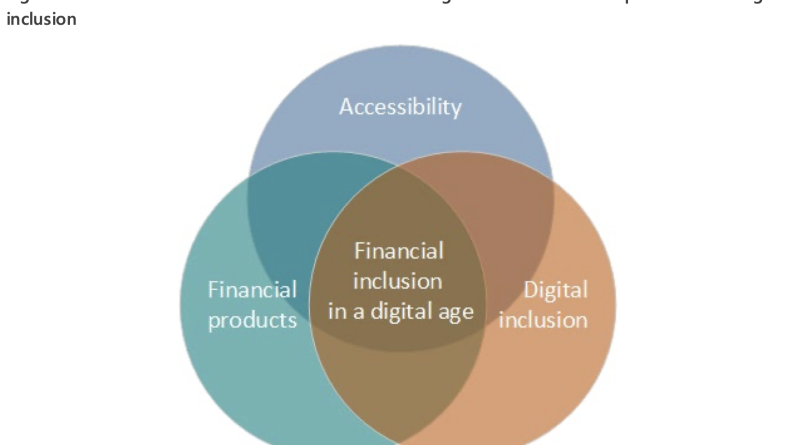

A typical argument made in favor of central bank digital currency (CBDC) is that it might increase financial inclusion. The nuances of how to accomplish that goal, or even what “monetary addition” implies, stay to be explored, a Bank of Canada conversation paper stated. By “recognizing product barriers and describing the truths of injustice underlying the aggregate statistics that are commonly utilized” the authors of the paper determined 3 types of addition required for an universally accessible payment method: financial addition, digital addition and useful ease of access. Cognitive load– the level of problem in using digital financial innovation– and other functionality issues are potential barriers to ease of access that are most likely to grow as the population ages.

A common argument made in favor of central bank digital currency (CBDC) is that it could increase financial addition. The subtleties of how to accomplish that objective, or even what “monetary inclusion” means, stay to be checked out, a Bank of Canada conversation paper stated. By “determining product barriers and describing the truths of inequity underlying the aggregate statistics that are frequently utilized” the authors of the paper recognized 3 types of addition essential for an universally available payment method: financial inclusion, digital inclusion and useful availability.

Cognitive load– the level of difficulty in utilizing digital financial innovation– and other functionality problems are potential barriers to ease of access that are most likely to grow as the population ages. Older people use smartphones less than more youthful and less than 60% of the population was assessed as having web skills that could be ranked advanced or skilled, according to a study mentioned. The problem needs “deeper research into style for cognitive availability,” the authors said.Related: Insurance, farming, realty: How asset tokenization is improving the status quoDisabled people might experience higher problem in utilizing the innovation as well. Handicapped individuals in Canada have substantially less access to the web than other Canadians.The challenge is in the shipment of services, instead of the nature of CBDC itself, the authors stated. Conquering those difficulties will require reserve banks to deal with problems that would otherwise be considered far from their scope of interest. The research study took a look at the needs of specific sections of the Canadian population. Due to the fact that of the high level of availability of financial services in the nation, a previous research study discovered that the majority of Canadians have little reason to utilize a CBDC. Magazine: Should you orange tablet children? The case for Bitcoin kids books

Related Content

- Police: Person shot outside North Carolina home of DaBaby

- Vitalik Buterin declares he is not staking all of his ETH, merely a ‘small portion’

- AI’s energy consumption concerns echo Bitcoin mining criticisms, says Heatbit founder

- Why I’ve Settled On The Electrum Bitcoin Wallet

- The Rise of Cryptocurrency: Everything You Need to Know