Ethereum price outlook weakens, but ETH derivatives suggest $1.6K is unlikely

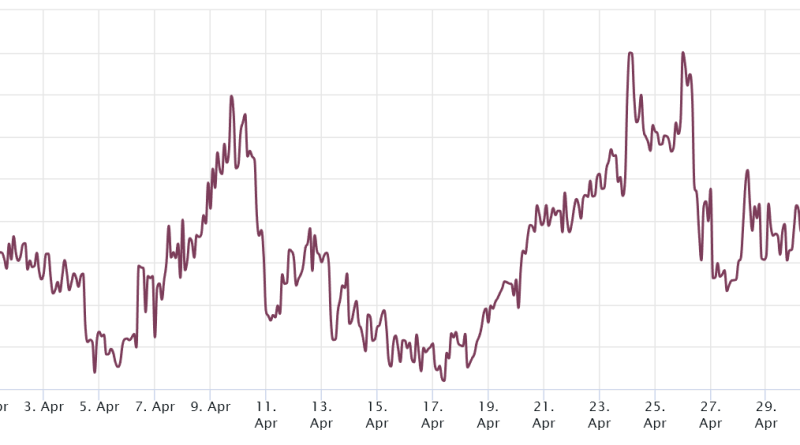

Source: LaevitasSince April 19, the Ether futures premium has actually been stuck near 2%, showing that professional traders are unwilling to flip neutral despite ETHs cost testing $1,950 resistance on April 26. As an outcome, traders ought to examine Ethers options markets to find out how whales and market makers value the possibility of future cost movements.Related: Venmo will enable fiat-to-crypto payments in MayThe 25% delta skew indicates when market makers and arbitrage desks overcharge for upside or drawback protection. Bullish markets, on the other hand, tend to drive the skew metric below 8%, showing that bearish put alternatives are in less demand.Ether 60-day options 25% delta skew: Source: LaevitasThe 25% alter ratio is presently at 1 as protective put choices are trading in line with the neutral-to-bullish calls.

” ETH cost overlooks banking crisisCuriously, the VIX sign, which measures how traders are pricing the risks of severe price oscillations for the S&P 500 index, reached its most affordable level in 18 months at 15.6% on May 1. It is worth noting that overconfidence is the primary motorist for surprise moves and large liquidations in derivatives markets, suggesting low volatility does not always precede periods of rate stability.The financial environment has actually gotten worse substantially after the U.S. reported first-quarter gross domestic item (GDP) growth of 1.1%, listed below the 2% market agreement. Investors are now pricing greater odds of a worldwide economic crisis as the U.S. Federal Reserve is anticipated to raise interest rates above 5% on May 3. Bullish markets, on the other hand, tend to drive the skew metric below 8%, indicating that bearish put choices are in less demand.Ether 60-day options 25% delta alter: Source: LaevitasThe 25% alter ratio is presently at 1 as protective put choices are trading in line with the neutral-to-bullish calls.

” ETH price overlooks banking crisisCuriously, the VIX sign, which measures how traders are pricing the dangers of extreme cost oscillations for the S&P 500 index, reached its most affordable level in 18 months at 15.6% on May 1. It is worth keeping in mind that overconfidence is the main chauffeur for surprise moves and big liquidations in derivatives markets, suggesting low volatility does not always precede periods of rate stability.The financial environment has aggravated considerably after the U.S. reported first-quarter gross domestic item (GDP) growth of 1.1%, below the 2% market consensus. Investors are now pricing greater chances of an international economic downturn as the U.S. Federal Reserve is anticipated to raise interest rates above 5% on May 3.